Hit enter to search or ESC to close

16 March 2026

Insurance Market Update - March 2026

Our recent market updates have highlighted the clear trend of insurance market conditions softening since Q3 2024.

Despite several weather-related loss events in New Zealand through 2025 and early 2026, the market remains soft in most areas which is good news for insurance buyers.

In 2025, global insured losses were 5% below the recent 10-year average, with natural hazards generating an estimated USD296 billion in direct economic costs. Of this, the private insurance market and publicly funded insurance entities covered an estimated USD129 billion. The remaining USD167 billion wasn’t insured, leaving a what is known as the protection gap, at 56%. Across the year, there were at least 58 individual events causing billion-dollar economic losses, with at least 23 of these also being billion dollar insured loss events.

Despite this, the (re)insurance industry enters 2026 in a very healthy financial position. Following consecutive manageable catastrophe loss years, there is a record amount, USD838 billion, of capital available for market deployment.

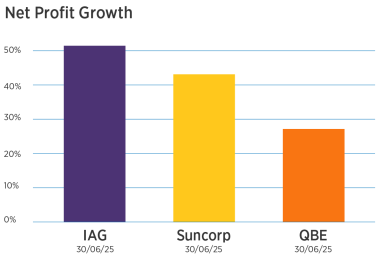

Locally, insurance companies have been reporting significant growth in profits. For the 12 months to 30 June 2025 IAG (which includes NZI, State and AMI) reported a 50% growth in profits, while Suncorp (which includes Vero and AA Insurance) exceeded 40% growth. QBE also reported a growth in profit of 27% in their half year in June 2025.

However, recent half year results show the first signs of pressure emerging from the soft market. Both IAG and Suncorp reported declines in New Zealand gross written premium. IAG’s intermediated business, which includes NZI, fell 10.4%, while Suncorp, trading as Vero in the New Zealand market, reported a 5.6% decline. As a result, both insurers also reported lower growth in profit for the period, although their underlying results remain strong.

It is worthy to note some of the comments made in the insurers’ own disclosures to the New Zealand market reinforce this trend. With IAG noting a “challenging New Zealand commercial market, with solid profit result reflecting ongoing underwriting discipline,” and Suncorp stating “GWP impacted by challenging market conditions in Commercial due to the soft market cycle.”

Here at Gallagher, we've certainly noticed that our New Zealand claims appear to be returning to "normal" volumes.

Additionally, the conflict in the Middle East has the potential to put pressure on global supply lines and costs such as oil pricing. This may well have an inflationary impact to claims, similar to what we saw through the Covid-19 pandemic and also in the initial stages of the Russian/Ukraine war.

Therefore, we anticipate there could be a tipping point at some stage in the next 6 months where decreasing premiums and normalised claims numbers cross over and the insurer profitability starts to decline which could trigger a flattening of the market. The first signs of this will be insurance companies becoming far more selective about which risks they offer pricing relief to.

This is a dynamic we are keeping a very close eye on.

New Zealand claims trends

Regular disruptive weather remains a driver of claims activity in New Zealand. For larger weather events insurance companies issue “event codes”, and in 2025 we saw 36 event codes issued. This resulted in 2,249 claims from our clients, representing 9.8% of the total claims for the year.

The current La Niña weather pattern, combined with warmer sea temperatures, is increasing the risk of tropical storms and severe rainfall events.

However, fires have recently been the cause of some of the major losses for our clients. These have included fires at supermarkets, schools, rugby clubs and recycling operations.

The most common causes of these fires is arson, hot works and lithium batteries, with the lithium-related incidents becoming increasingly common due to wider usage and often resulting in significant damage.

Cyber incidents also continue to rise in both frequency and severity, resulting in operational disruption, financial loss, and reputational damage.

We are seeing losses spread across multiple attack types including business email compromise (BEC), payment fraud (e.g. bank impersonation), ransomware, network compromise and privacy and data‑handling breaches by employees. The breadth of incidents highlights the persistent and evolving nature of cyber risk.

Vehicle theft is also on the rise due to the availability of devices that can bypass keyless ignition systems. Compounding this, the growing number of new vehicle brands that are entering the market with parts that are difficult to source (often Chinese manufacturers that haven’t built up parts supply and networks yet), is resulting in longer repair times and extended claim durations, which ultimately increases claim costs.

There is good news though. In our experience we’ve seen the average time taken to settle a claim reduce by nearly 55%. This is reflective of advances in online claims lodgement tools and the digital interface between Gallagher and insurers.

The AI evolution brings risks as well as rewards

When generative AI first burst onto the scene in November 2022, it sparked a wave of excitement, curiosity and anticipation. The possibilities seemed endless.

Fast forward three years, and while the initial buzz remains, a sense of realism has settled in.

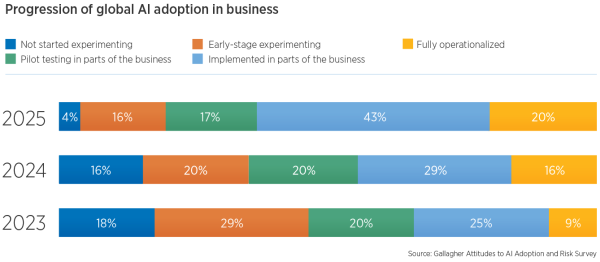

According to Gallagher's latest research, adoption of generative AI has continued over the last year, with many organisations now shifting their focus beyond determining which AI tools to adopt and instead focusing on how to operationalise the technology within the business.

The 2025 Gallagher Adoption and Risk Survey showed that in the past 12 months, the rollout of AI adoption strategies has accelerated, with a much greater proportion of businesses (63%) now having either fully operationalised or implemented AI within parts of their business, a marked increase from 45% in 2024.

Currently, the most popular uses for AI are in IT operations management, client-facing functions such as chatbots and personal assistants, and research and analytics.

Whilst the possibilities of AI seem extremely enticing, the use of AI does come with risk. The survey showed that AI errors, misinformation and hallucinations remain a key concern, topping the list of perceived threats from AI adoption (57%), as do legal and reputational risks from AI misuse (56%) and data protection and privacy violations (55%).

People-related risks also remain a top concern for business leaders in adopting AI. At least half of businesses see potential job insecurity as a side effect of AI transformation, alongside a drop in employee engagement and change fatigue. If left unaddressed, these issues could prompt reduced trust in leadership.

Furthermore, respondents highlighted the importance of recognising the potential negative impacts on the workforce and emphasising the need to involve HR in addressing employee concerns. They also stressed the value of offering training programs to help employees adapt and feel supported through the changes.

Speak with your Gallagher broker to get a better understanding of how your use of AI may impact your risk exposure.

Legislative changes to prepare for

As outlined in the last insurance market update, two significant legislative changes will come into effect in 2026.

The first is the Resource Management (Consenting and Other System Changes) Amendment Act 2025, which is intended to support the transition to a new resource management system and to strengthen the RMA’s compliance and enforcement regime.

The second is the upcoming change to the Fire and Emergency Service New Zealand (FENZ) levy, including revised levy rates and updated application rules across different property types, which will take effect as of 1 July 2026. Please review our Client Advisory for a detailed breakdown of the new requirements.

Our brokers are available to guide you through these changes and explain any impact on your insurance coverage.

Be sure to engage with your broker to discuss tailored insurance solutions which optimise your coverage and leverage the current market conditions.

Download FENZ Levy Client Advisory