Hit enter to search or ESC to close

Risk Management Climate Change

25 May 2026

The impact of climate on insurance and risk to your business

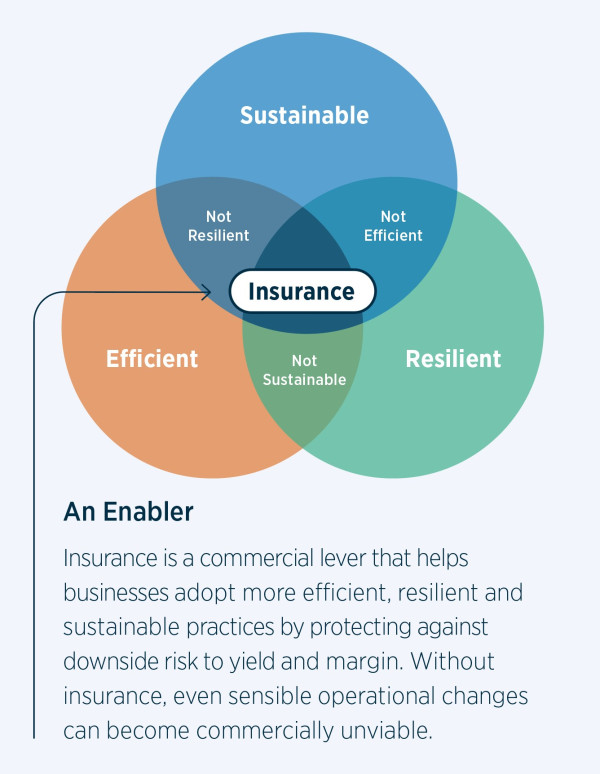

New Zealand businesses are under pressure from multiple directions at once. They are being asked to operate efficiently, strengthen resilience and meet rising sustainability expectations, all while margins are tightening.

Each of these objectives can work against each other. Sustainable practices often require upfront capital. Lean and just‑in‑time models reduce buffer and spare capacity, leaving less room to absorb disruption if something goes wrong.

At the same time, climate‑related risk is increasing in both frequency and severity, putting pressure on businesses to act quickly, often with less time and flexibility to weigh options, making decision-making more urgent and more difficult.

Gallagher works with New Zealand businesses to understand their exposure to natural hazards, structure insurance programmes that reflect that exposure, and build resilience that can be evidenced to insurers, lenders and investors.

The data shows what matters now

This is no longer a future risk. The impact is already visible in insurance and loss data across New Zealand and Australia.

IAG’s Wild Weather Tracker (April 2026), covering the 12 months to the end of February 2026, reported:

46storms in the 12 months to Feb 2026 (up from 29 the prior year) |

33,174storm-related claims to IAG brands (up from 9,324) |

256%year-on-year increase in storm claims |

1 in 8days saw a damaging storm — up from 1 in 19 over 15 years |

In New Zealand, three events drove much of this increase. The October 2025 South Island windstorm, the February 2026 lower North Island storm, and in April 2026 ex‑Tropical Cyclone Tam. Each event affected thousands of businesses simultaneously, overwhelming suppliers, trades and loss adjusters.

The pattern is not unique to this market. In Australia, extreme weather events generated AUD $4.8 billion in insured losses during 2025, a 727% increase on the prior year. Globally, Munich Re attributes 92% of natural catastrophe losses in 2025 to weather‑related events, with insured losses exceeding US$100 billion for the seventh consecutive year.

This impact can still influence premiums in the current soft market and even for organisations with no recent claim history. Insurance markets are responding to a global weather signal, not just individual loss performance.

Resilience is a commercial asset and you can build it deliberately

Businesses that act early on climate and natural-hazard risk are finding that the benefits extend well beyond insurance alone. Lenders increasingly factor physical climate risk into financing decisions. Government and corporate customers expect suppliers to demonstrate continuity and resilience as part of procurement. Investors assess climate-related disclosures to understand long-term durability. Insurers respond to the same evidence when setting terms, capacity and pricing.

The work you do to understand and manage exposure supports every one of these conversations.

What you can do

Start by developing a clear view of where your business is exposed — across physical locations, supply chain concentration, long lead-time equipment and single-source dependencies. That clarity provides the foundation for decision-making.

From there, you can make deliberate choices about which risks to reduce, which to retain, and which to transfer, and demonstrate that approach to lenders, customers and investors in terms that are relevant to each.

Insurance is part of that framework. A well-structured programme supports necessary operational trade-offs and helps ensure that decisions made for efficiency and competitiveness remain financially resilient. It protects the downside, supports access to capital, and provides a pathway to recovery when disruption occurs.

Where Gallagher fits

Our role as your broker is to work alongside you throughout the year, so when the next climate event inevitably occurs, the insurance programme behind your business is already doing its job, as part of a resilience strategy built to last.

How we help

Start with exposure

1. Site level exposure assessment

Using current New Zealand data, including council hazard portals, NIWA data, and flood and coastal models. We develop a credible baseline view of flood, coastal, liquefaction, wind and wildfire exposure across every site.

2. Risk tolerance assessment

We help define what your balance sheet can absorb, what would hurt, and what would threaten viability. This informs appropriate deductibles, limits and insurance programme structure to help avoid both unnecessary spend and unacceptable exposure.

3. Sums insured and recovery assumptions

Declared values, sub limits and indemnity periods are tested against current rebuild costs and realistic recovery timeframes. This is often the fastest way to improve the likelihood that cover will respond as intended.

Then build resilience around it

Business interruption financial assessment — our in-house forensic accountants model realistic Business Interruption (BI) loss scenarios against your actual financial profile, turning a BI sum insured and indemnity period into a defensible figure.

Critical asset and supplier review — we map your operational dependences to identify single points of failure across plant, equipment and tier-one / tier-two suppliers.

Risk engineering and evidence packs — we document mitigation measures to clearly articulate your risk profile and improvements, helping to accurately price your insurance into the market.

Advanced insurance structures — we design tailored insurance programmes to address complex risks, which can include parametric cover, contingent BI and layered catastrophe programmes.

Governance and board-level support — we translate exposure data translated into clear insights for directors, lenders and investors. This includes framing financial impact, risk tolerance and mitigation strategies.

Recovery and claims readiness — we put practical protocols in place before an event including preferred loss adjuster, pre-documented asset register, and 72-hour protocols.

How this works in practice

We’ve helped businesses across a range of industries understand exactly where flood risk sits within their portfolio and supply chain.

We identify the most vulnerable sites — ranked by flood frequency and depth so clients know exactly where their real exposure lies.

We turn that insight into action — prioritising interventions like flood barriers, drainage upgrades, and infrastructure improvements to ensure capital is spent where it has the greatest impact.

Where immediate mitigation isn’t possible — we identify insurance gaps relative to actual risk, ensuring cover is appropriate until longer-term works can be delivered.

The outcome is a clearer, prioritised view of risk, supporting better allocation of capital, more informed insurance decisions and a more resilient operating model.

Risk is being re‑priced at your property, not your sector

Insurers increasingly assess flood, coastal and weather exposure at an individual site level, alongside rebuild costs. Two otherwise similar businesses can face very different terms based solely on location‑specific data.

A documented exposure assessment, supported by evidence of mitigation, is often what influences pricing, capacity and terms.

The true cost of risk now extends well beyond premium alone. Higher deductibles, tighter sub‑limits, working‑capital strain from below‑deductible losses and longer recovery periods are all part of the equation but if managed well, these impacts can be stabilised.

Much of this exposure is not new

Flood plains were flood plains decades ago. Coastal sites have always faced storm surge. Single‑supplier dependencies have long been fragile.

What has changed is frequency, severity and visibility. Climate risk is accelerating conversations that were already overdue.

If your business is exposed today, climate change is not the starting point, it is the prompt.

Before investing in mitigation or restructuring an insurance programme, we recommend understanding your exposure across sites, assets and supply chains today and as conditions change. Every other decision with the help of your broker flows from this.

Download this article here.

Your next step

Don’t wait for climate pressures to force your hand. If your business is already exposed, the conversation has already started.

Talk to your broker to arrange an initial discussion about your risk exposure. This will help you understand what to prioritise ahead of your next insurance renewal, and what steps to start taking now to reduce risk.